R N Bhaskar

13 July 2015

There are signs of gloom. People have already begun grumbling, even accusing the government of causing a slowdown. A major pointer is the dipping flow of investments into India. Is the Indian economy sinking?

Maybe not. There are good reasons to suggest that this gloom could be short-lived. For several reasons.

First, the global slowdown in investments began much before the present government came to power. India, too, moved in tandem. However, unlike others, India could buck this trend this year.

Second, remember that an economic slowdown is inevitable when there is a large-scale crackdown on big corruption. This is because when the flow of easy money gets stanched, the first casualties are invariably clubs, pubs, restaurants, cabs and airlines — where such money gets sloshed around.

Faith in specious logic then prevails. But that is like justifying the existence of a monarch who squeals, “If you do away with me, what will happen to my 300 concubines? My 1,000 servants? The gardeners? The advisors?”

For those affected, the clean-up exercise is traumatic. But this exercise eventually allows for healthier, more equitable and sustainable growth.

Consider some of the moves already initiated (some taken from Ambit Capital’s May 15 report):

Civil servants and public sector company chiefs have been pressured to deliver, and to desist from graft (watch the manner in which their daily attendance and activity is monitored at www.attendance.gov.in). Criminal prosecutions have been launched against executives from prominent oil & gas, steel and power companies. More high-powered measures against corruption are contemplated.

Crony capitalists and contractors have been compelled into re-thinking their traditional approach of rigging the system. The auction of telecom spectrum and coal mining licences bear testimony to this fact.

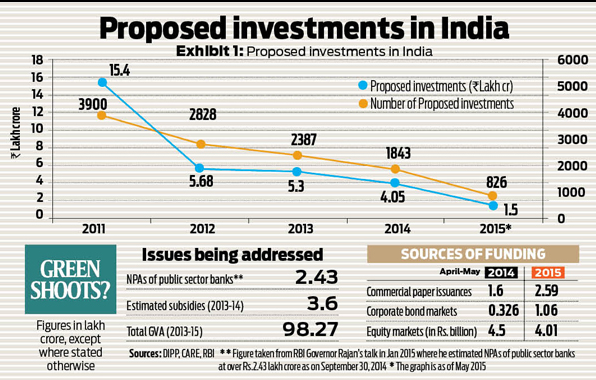

Subsidy related fraud is being attacked through the Direct Benefits Transfer (DBT) and the Aadhaar route. This has already been done for LPG (cooking gas). Now the PDS (public distribution system) is also being linked to DBT in a phased manner. That should help rein in subsidies, which have crowded out money for development (see chart). Remember, almost 85% of the Rs3.6 lakh crore worth subsidies does not reach the target recipients.

When money reaches the right people, consumption demand should rebound.

The crusade against black money has just been launched.

The gold bond scheme hopes to bring at least Rs15,000 crore into productive channels.

All these measures have hit the grey world’s market intermediaries. That in turn has affected consumer spending. Expect some more pockets to get emptied, which in turn will cause some more pain.

But that is where the third measure becomes important — the flow of investments, for fresh job creation. Expect this flow to increase — most particularly from Singapore, Japan, Germany and Australia. Investments from China have yet to play a significant role. Similarly, expect development of coastal areas to gain momentum.

Fourth, the restructuring of India’s public sector banks will also be painful, as they are forced to clean up their non-performing assets (see chart). But that could spur greater professionalism within the banking sector. Lastly, observe other interesting numbers. True, amounts raised through public issues have shrunk (see chart). But that has been more than compensated for by bond markets and the issuance of commercial paper. Translated, this means that investment money for new projects, and new jobs, has just picked up pace, though through non-conventional financing.

As Akash Prakash of Amansa Capital points out, “Roads are getting on track. Officials feel confident that more than 10,000 km would be ordered and over 6,000 km built in 2015-16 (compared with 4,000 km in 2014-15). Of the 80 road projects stuck when the NDA took over, only 20 remain, with 16 projects being taken over by the NHAI, and many being cancelled and re-tendered.”

Similarly, addressing India’s vexatious labour laws (left unchanged for 20 years) has just begun. Link these to other measures aimed at easing the way of doing business (GST is one key measure) and the fog begins to lift.

A critical area that remains unaddressed is power distribution and power subsidies. And some measures like the beef ban are certainly unwanted, and uncalled for.

More worrying is the tendency of the human resources ministry to focus on tinkering with good institutions instead of focussing on primary and secondary school education where the rot really lies. But more on that later.

Sectors like real estate will continue being under pressure for some more time (another unfortunate victim of the crusade against black money).

As Sajjid Chinoy (chief India economist at JP Morgan) points out, “Capital goods production has increased smartly within the IIP (Index of Industrial Production) and is averaging 10 per cent over the last three months, a consistency and level not seen since the spring of 2011.” This, he adds, is corroborated by sales growth of capital goods companies in the BSE 100, averaging 10-11% over the last two quarters, lending credence to the cap-goods production lift.

Not surprisingly, even while downgrading global growth, the IMF last week upgraded India. Its GDP growth is expected to surpass China’s. Clearly, there should be a lot to cheer about soon.

The author is consulting editor with DNA.

Read the original article here.

{kind=link}

COMMENTS