Oil to pressure remittances into India?

http://www.freepressjournal.in/oil-to-pressurise-remittances-into-india-r-n-bhaskar/767163

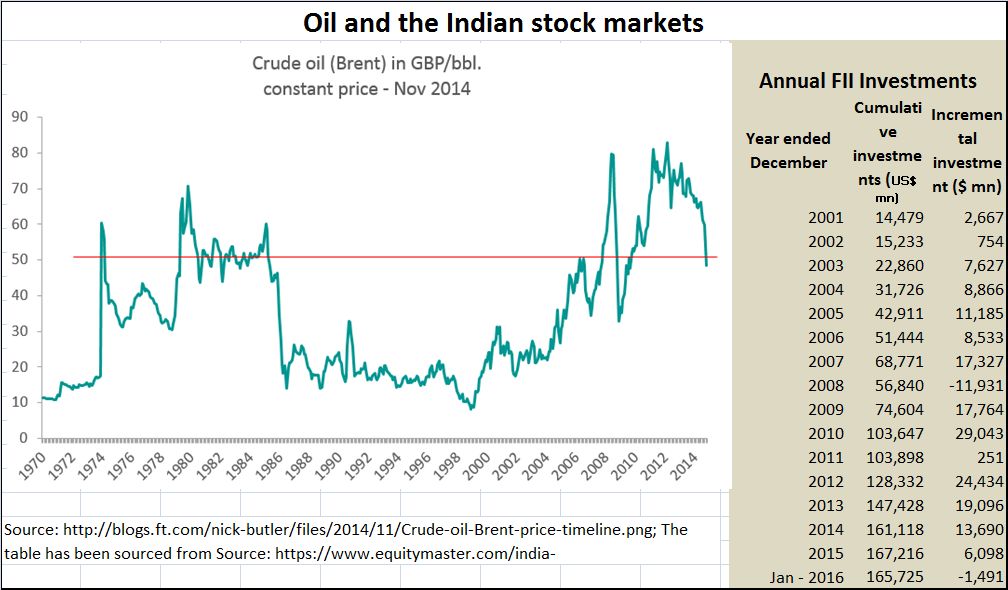

Oil slipped below the psychological barrier of $30 per barrel last week, sending out gasps of shock and amazement. Few had expected it to fall below the $40 level. But the markets had defied such expectations. Some, like Goldman Sachs, expect it to fall to $20. Déjà vu! It could be the 1980s and 1990s all over again (see chart).

Till that time, there was a pious belief that the fall in oil prices would benefit, not hurt, India. After all, each drop of $1 in oil prices reduces India’s import bill by 1 billion rupees (100 crores) a year. The cumulative impact of falling oil prices has been estimated at over Rs. 5 lakh crore. That has helped India manage its Current Account Deficit (CAD) and its Balance of Payments (BOP). But this slide below the $30 mark sent shivers down the spines of most marketmen.

They knew that this could mean the start of a huge bearish trend in the Indian stock markets. That could affect capital formation, as less money would flow towards financing new projects. In turn, this could dampen employment generation, a crucial issue with the government. Its very political survival depends on economic growth and employment generation.

Predictably, after a long time, net foreign institutional investments (FII) turned negative by January, see chart). And the reasons were not hard to find. Much of the FII money coming into India are through mutual and hedge funds. The US alone accounts for almost $1 trillion as investments into emerging market (EM) funds. Except for a few funds in Europe, none of them are India designated funds.

Being part of the EM group was good so long as all EM countries were on an upswing. But now, almost every EM country is limping. They have got badly bruised by the fall in commodity prices. China is experiencing a slowdown which has sucked the breath out of global demand. Even the BRICS grouping had become irrelevant.

Not surprisingly, hot money – often believed to be politician-related funds – also became skittish. According to SEBI data, the total value of Participatory Notes (PN) investment in Indian markets (equity, debt and derivatives) declined to Rs 2,54,600 crore at November-end, from Rs 2,58,287 crore in the previous month. Expect this to fall further.

Ironically, India was supposed to be in a sweet spot, as one of the best performing emerging economies. But the falling price of oil began hurting the oil producing countries. They, in turn, opted to pull out monies they had invested with investment managers. The weakest performing funds were those which had invested in emerging economies. Over a 10-year period, the returns were almost zero. During the last five years, the return was a minus 20%. It was, therefore, inevitable that these funds would be pulled out. Without the life blood support of money, stock market indices are bound to fall.

That is why, marketmen have begun hoping that the government allows some of the domestic funds to get invested in Indian markets. The biggest investible money is with the LIC. But there are pension funds and provident funds. Can they be deployed?

Sounds logical. But not with the existing corporate governance norms. Look at the way in which money was disbursed by banks. Anyone with a bit of common sense could have realised that there is no way electric arc furnaces could compete with coal based furnaces. Yet the banks gave away money to such steel plants. The biggest loan went to Bhushan Steel, which is today in danger of being written off. Ditto with some reckless loans — to politically well-connected groups — bidding for solar and thermal power projects.

Investing provident and pension funds in such companies may not be a good idea. The only way out will be to introduce legal provisions enabling citizens to urge prosecution against elected representatives, bankers and even bureaucrats where there is ample evidence of active connivance, or the passive turning a blind eye. SEBI and Indian courts need to take a firmer stand against corporate mergers, demergers and delistings which are patently against investors and ethics. Good regulation of the stock markets still has a long way to go.

And there could be more pain ahead. The fall in oil prices has begun hurting employment in the Middle East and elsewhere. Banks in the UAE have cut almost 1,500 jobs. This is not confined merely to the likes of Standard Chartered and HSBC. It has extended to local lenders. Barclays Plc. reportedly plans to cut 250 of 1,000 planned job cuts in Asia. And Morgan Stanley is cutting 1,200 workers worldwide. Schlumberger plans cutting some 34,000 jobs worldwide.

Expect remittances into India to be under pressure, unless the government manages to strike deals for reconstruction contracts in Iraq, Afghanistan and Syria. A deal with Russia will help enormously, as it wants people to exploit its mines – especially gold – at low costs. India can play a significant role. But it needs imagination and economic negotiation skills on the part of the country’s policy makers.

Will India be up to it?

Finally, what will the future of oil be? And what are the options before the Indian government? What this space.

{kind=link}

COMMENTS