http://www.freepressjournal.in/recounting-the-great-indian-bank-robbery-rn-bhaskar/789412

http://www.freepressjournal.in/recounting-the-great-indian-bank-robbery-rn-bhaskar/789412

Recounting the great Indian bank robbery

Feb 25, 2016 02:13 am

The biggest players, goes a common saying, are often the most shameless. This was reinforced when data came rolling out of the presentations made last fortnight by S.S.Mundhra, deputy governor, Reserve Bank of India (RBI).

It also explains why the Supreme Court too has decided to step in and ask the RBI to disclose the names of the biggest defaulters.

It also explains why the Supreme Court too has decided to step in and ask the RBI to disclose the names of the biggest defaulters.

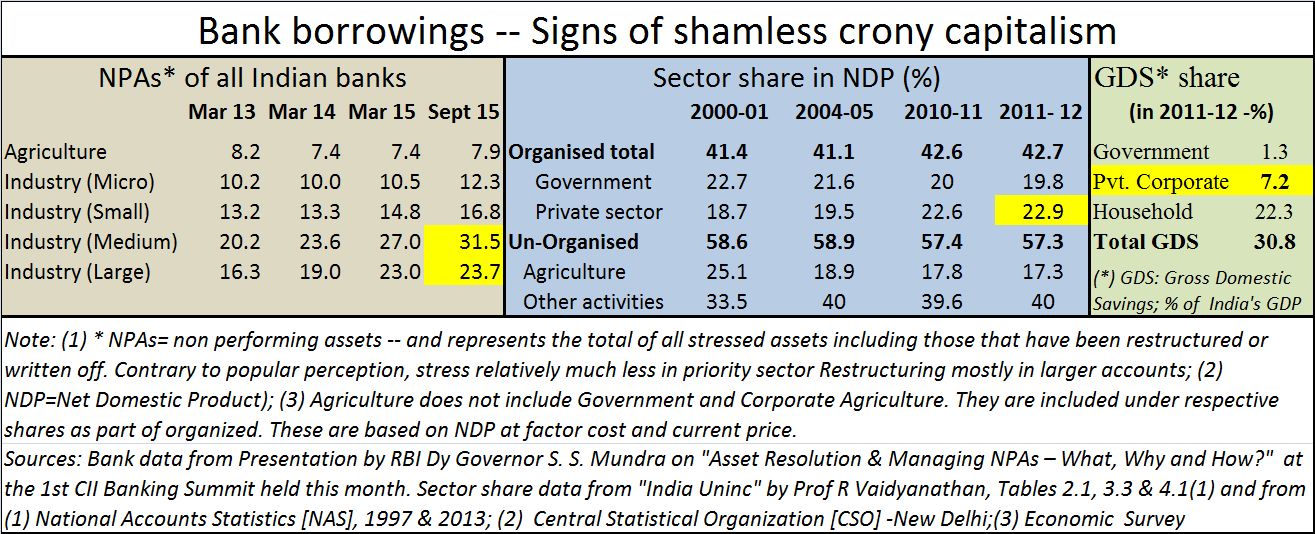

RBI’s data shows that medium and large industrial players accounted for over 55% of the stressed assets faced by banks. These are the players who account for just 23% of India’s net domestic product (NDP) and less than 10% of its workforce. Compare this with loans taken by the agriculture sector. Even though it accounts for over 50% of the country’s workforce, and contributes to over 17% of its NDP, agriculture accounts for just 7.9% of NPAs (see chart).

In fact, the agricultural sector highlights a crucial aspect about India’s value system. For the past four decades, India’s politicians have constantly tried to teach farmers and rural folk not to repay loans. It started with the infamous loan melas started by Prime Minister Indira Gandhi – a move that almost bankrupted the country’s banks and set the path for the country’s financial woes in the early 1990s. Despite this lesson, legislators have opted for loan waivers every now and then.

This is always worrisome, because a section of India’s legislators has actually been trying to corrupt the most creditworthy community in the country. Rural folk, conventionally, have been god-fearing and honour-bound. They consider it a matter of pride and honour to be capable of taking over and redeeming the debts of parents and close relatives. They have often believed that non-payment of loans brings dishonour to the entire family.

When legislators teach farmers not to repay loans, they are attempting to render dishonest the nation’s most creditworthy sectors. They also encourage, simultaneously, the most corrupt among large and medium industry players. Mercifully, despite such corrosive attempts by some legislators, the farmer has remained India’s most credible borrower. His contribution to stressed assets is the smallest.

Now, consider the role of medium and large industry. Its contibution to jobs in the labour workforce is poor (under 10%). Its share of gross domestic savings is pathetic. Almost two-thirds of the gross domestic savings of this country came from the household sector. The private corporate sector’s contribution was less than one-fourth.

Moreover, contrary to justifications claiming that the surge in NPAs was on account of the downturn in the global economy, much of the blame lies elsewhere.

Consider the manner in which banks gave away money to steel mills that were located in the worst places — far from ports, from coal, or even iron ore. Steel is a freight sensitive commodity. It does not need a Harvard gruaduate to tell a banker that a steel unit located far away from raw material or fuel sources cannot be viable. Yet banks gave money for setting up such units. Just one such industrialist has totted up bad debts requiring restructuring of loans of over Rs.30,000 crore.

Look at another industry group that sought to exploit and refine oil, but whose gross refining margins were always lower than those of its peers. That group ended up borrowing over US$18 billion – both from foreign and Indian banks – without affected bankers asking the right questions. The group was large. Its track record of bribing government officials, legislators and even journalists is by now legendary. Will the Supreme Court now be compelled to ask the questions that bankerts forgot to ask?

Look at a third instance where bankers have lent big sums for building a port and for landbanks for a smart city to people with few linkages in the port business.

The list can go on.

Sadly, one of the big obstacles in even recovering these sums is the absence of a bankruptcy code. The legislators who were quick to hike their own perquisites, failed to legalise this crucial facility.

Each of these groups – like so many others – was politically well connected. Each of them hoped to make money by persuading bankers, legislators and bureaucrats to further bend the rules in order to make their projects viable. Subsequently, more money was lent to help these groups pay interest on the original sums borrowed. Thereafter, more money was lent to avoid the risk of losing public money (all public sector banks use money belonging to taxpayers and depositors). When the burden became too large, loans were written off. Most of the time, it was the public sector banks that lent out more money generously – it is easy to be generous with other people’s money (http://www.freepressjournal.in/when-banking-becomes-a-nightmare-rn-bhaskar/777519).

The RBI data thus suggests that the future of good banking lies more in the hands of small enterprises and rural folks than with large enterprises. This is why people like Prof R. Vaidyanathan defend the “unincorporated” (in his book titled “India Uninc” http://asiaconverge.com/2015/08/story-of-unsung-unincorporated-india/). They view large players as leeches that have learnt to prey on public money.

Hence, the Supreme Court’s scrutiny of large borrowers is welcome. It’s time big unscrupulous industrialists went to jail, or are compelled to repay bank loans. It’s also time for big bankers to be asked why they failed to ask the right questions. Was it incompetence? Or was it collusion?

{kind=link}

COMMENTS