https://www.outlookindia.com/magazine/story/then-a-mundhra-now-a-mallya/299122

If you want to rob everyone, just start a bank

R.N.Bhaskar –

There is an old saying which puts it quite pithily: “If you have a gun, you may be able to rob a bank; but if you own a bank, you can rob everyone.”

It applies to Indian banks as well. Remember bank nationalization? Loan melas? Collusive deals with defaulting borrowers? In all such cases, legislators forgot that money must be earned. That money cannot be frittered away. Unfortunately, the banking regulator did not draw the red line before the deluge began. Unfortunate too that the regulator’s inability was not challenged by the courts in time.

In fact robbing people through banks has taken three forms.

The first involves raising deposits from trusting, unsuspecting people, then giving out loans to a close coterie of friends, and then going bankrupt. The world has seen it. So has India. The Justices Tendolkar/ Vivian Bose report of 1963 on the Dalmia-Jain group of companies (http://reports.mca.gov.in/Reports/18-Tendolkar%20committee%20report%20of%20the%20commission%20of%20inquiry%20on%20the%20administration%20of%20Dalmia-%20Jain%20companies.pdf) actually documents how this was done.

Then take the second way of robbing people. This happens when governments own banks. That is when politicians begin to think that the money with government-owned banks is their own money. They think they can give away money to those they favour most. That is what happened with loan-melas in the 1980s.

Then take the second way of robbing people. This happens when governments own banks. That is when politicians begin to think that the money with government-owned banks is their own money. They think they can give away money to those they favour most. That is what happened with loan-melas in the 1980s.

In India it has happened time and again – even before banks got nationalised. But government-owned Life Insurance Corporation (LIC) was around. That is what led to the emergence of the celebrity status Mundra scandal (it was exposed by Feroze Gandhi, husband of Indira Gandhi). LIC was prevailed upon by the then finance minister (FM) to lend to Haridas Mundra money against shares (and bogus shares). The FM thought that the prime minister (PM) wanted this done. The deal was abetted by the Reserve Bank of India (RBI).

All the four offices were later embroiled in another scandal with another HM (Harshad Mehta) a full 37 years later. Like before, the PM, FM, RBI and the financial institutions were involved.

There was one difference though. When the Haridas Mundhra scandal broke, Justice MC Chagla ensured that the public had a right to know how financial crimes take place. The FM, RBI governor and LIC chairman were asked to depose before an open court. So large was the audience, that people had to sit on the lawns where loudspeakers were set up. The FM resigned. Mundhra was sentenced to prison (though he got away without anyone knowing by placing a benamidar in the prison to impersonate him). Soon, protective walls were built around public servants and politicians. Public trials were no longer possible.

Then you have the notorious Nagarwala scandal of 1971. It related to several trunks of cash suddenly disappearing from a nationalized bank. There was panic as the banks realised that they had been gulled. When traced, Nagarwala admitted that he had indeed taken the money. He was arrested, but the bank manager was not. In fact, it was the bank manager who took the money from the bank and gave it to an unknown man, on the basis of oral instructions that the manager thought had come from the PM’s house. The unknown man was Nagarwala, who put the money into a cab in the manager’s presence and sped away. Nagarwala demanded that the manager be investigated. Before this could be done, the young officer in charge of the investigations died mysteriously in an accident. Nagarwala then decided to speak to the media. But before this could happen, he was rushed to a hospital in a serious condition. He died in the hospital itself. A commission of enquiry was appointed. Nothing happened.

Today too ministers are seldom arrested for instructing bankers to give away the money to someone else. Occasionally, bank managers get arrested. For instance, nobody has asked for the arrest of the person who instructed banks to give loans to Mallya against the Kingfisher brand name. Similarly, nobody has asked for the head of a minister whose role was highlighted in an official verdict issued by a Canadian court. It was about bribes paid to Air India. Today the bad debts that Air India is reeling under are also burdens that Indian banks – and therefore Indian taxpayers – have to bear.

Everyone knows about politicians skimming money off cooperative banks. The RBI too knows this. But it keeps silent. And seldom do the courts ask why.

But now there is a third way to rob people. . . By defrauding small customers in a million ways. It is death by a thousand cuts, says a cynical observer of the financial sector. What makes this method more dangerous is that it enjoys the garb of legality.

Take a good example. Most people don’t realise that their money is their money only as long as it is in their pockets or in their own vaults. You are then the owner of your own money. But once you put it into the bank, you only remain the notional owner. On the bank’s books you become a sundry creditor, nothing more. So when a bank has to close down, secured creditors (other banks and the government) get their money first. Only the dregs – if there are leftovers — may reach depositors. Usually, the depositors get nothing.

Oh yes, there is deposit insurance. But that is limited to Rs.1 lakh per depositor (irrespective of the amount deposited). So if you were a pensioner who had put his life’s savings of Rs.10 lakh in the bank before it downed shutters, you would get only Rs. 1 lakh. Kiss the remaining Rs.9 lakh goodbye! The insurance cover is pathetic.

Customers seldom realise their vulnerability, till their money is gone. This is what happened to the depositors of Kapol Cooperative Bank once it was shut down.

The good thing here is that your money is relatively safe with nationalized banks. No nationalized bank – to the author’s knowledge – has ever closed down. If the losses are too big, it gets merged with another bank. The loot is seldom recovered. So if you want to keep your money safe, you are better off with a nationalized bank than a private bank.

Till of course, the nationalized banks also begin to emulate the ways of private banks and think that they can make money by charging customers additional sums for the services they are being given. This way, you begin to skin customers even while their deposits are relatively safe with the banks.

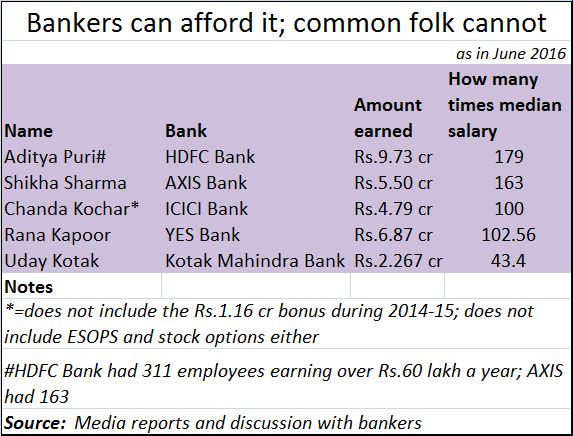

The signal appears to have come from private banks. One senior banker, Aditya Puri of HDFC, went on record stating that he had to charge more for the bank’s services because he had to take care of other stakeholders. He should have been reminded that if the ‘other stakeholders’ put in Re.1/- the remaining Rs.9 in a bank come from depositors. Thus the depositors are larger stakeholders. You cannot penalise the depositors just because 10% of the stakeholders want higher returns. And the bank management makes money on the money that depositors gave to banks. The management makes money far in excess of the median salary (see table).

The top management of nationalized banks are paid considerably less than their private bank counterparts. But they too have begun to eye bigger revenues.

One solution would be to allow account portability. Thus a customer can transfer to another (better) bank his account (or loan account) – along with all relevant instructions given to the original bank. The RBI agrees. But the FM appears unwilling,. Banks will drag their feet. Just the way mobile phone companies did.

In fact, the entire situation is farcical. When ATMs were introduced, customers were persuaded to use the ATMs because they would enjoy 24-hour banking, and save the banks some money. Now when the customers are getting used to ATMs, the banks want to charge for their use,

Then you have the prime minister exhorting people to adopt digital banking. And just when they begin to embrace it, the banks tell them that there will be charges levied on digital payments as well. Banks have discovered new ways to to rob everyone. Earlier, it was only politicians who were playing this game. Now it is the turn of every bank.

Ideally, the RBI should have put a stop to it. And when RBI failed, the courts should have drawn the line. The first capitulated. The second remained a bit hesitant. In fact, the few times the RBI has actually moved is when the courts stepped in. This time the apex court – none less – has asked for details of loan defaulters. The pressure has become so great that both politicians and the RBI have begun to wilt. Since the courts enjoy this power, the politicians are now keen to trim the powers of the courts. Fortunately, this hasn’t happened till now.

But a lot more needs to be done. Will the RBI move fast and remedy the situation?

{kind=link}

COMMENTS