https://www.moneycontrol.com/news/business/opinion-the-increasing-relevance-of-gold-3915741.html

The increasing relevance of gold

RN Bhaskar — 1 May 2019

During the past decade many central banks have opted to purchase gold and shore up their gold reserves. This is in contrast to the previous decade when many central banks actually sold gold. So is something happening?

The move by central banks has in turn made gold speculators in Dubai quite bullish. Many of them, under the condition of anonymity, talk about a bull run on gold. The timing is never certain, but they are betting that gold prices could move up as much as 10x, not just a few percentage points. It needs to be underscored that the objective of this column is not to recommend gold purchase, (all speculation is always fraught with risk) but to point out the ripple effect central bank gold purchases have caused.

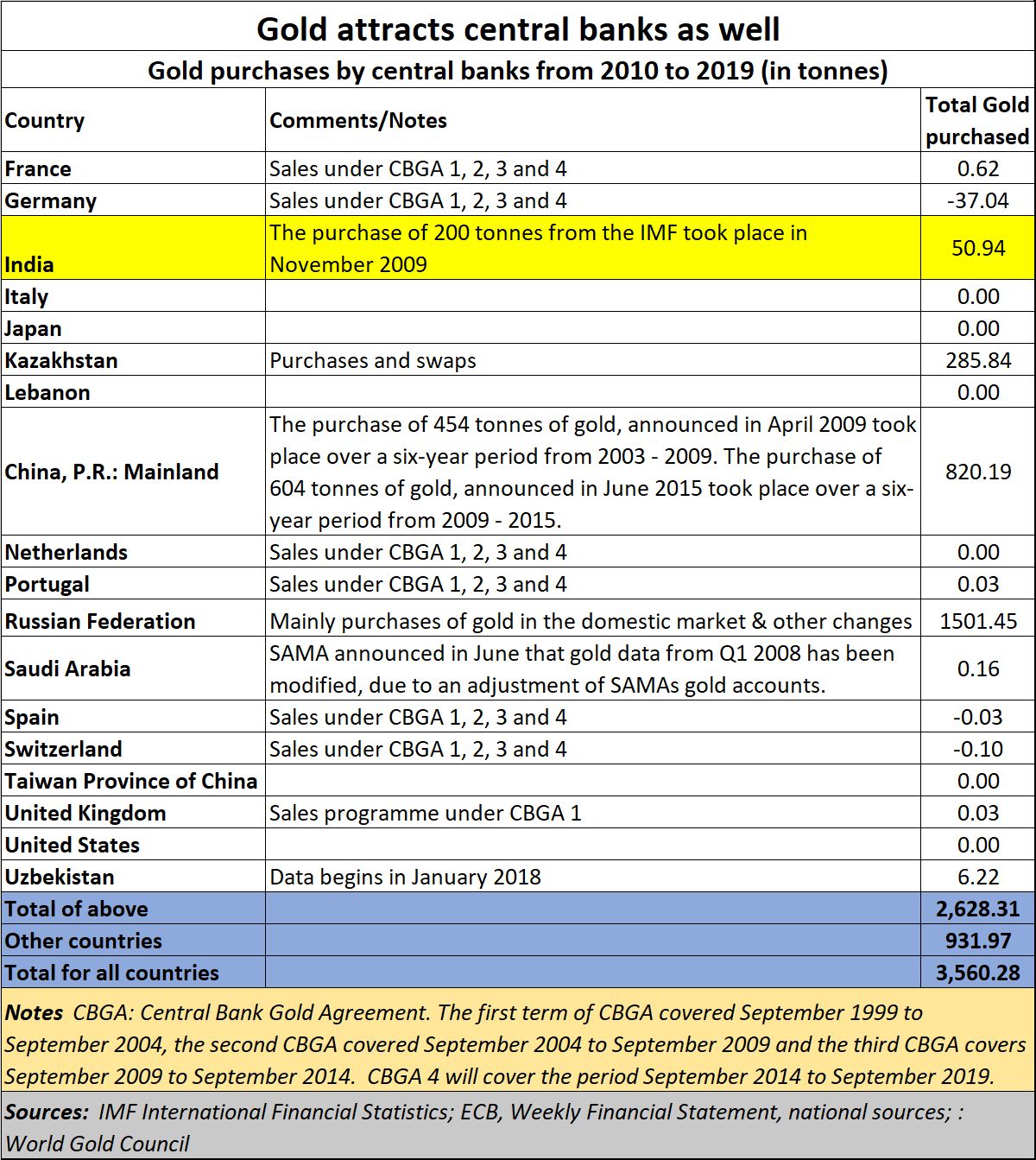

The fact that gold is being purchased by central banks cannot be denied (see chart). The only exception was Germany which sold 37 tonnes. Between 2010-19 total gold purchased by central banks was 3,560.28 tonnes. Of this, just the top 18 gold owning central banks accounted for purchases of 2,628 tonnes. The biggest among them was Russia, followed by China. India too purchased 50.94 tonnes.

But why were central banks purchasing gold? The standard answer given by central bankers that gold is part of a basket of currencies that each country has to form, as part of its foreign exchange reserves. Many countries found it prudent to increase their holdings in gold.

But the unstated reason is always around. Many countries have begun to suspect that holding too many US dollars as part of their reserves might be unwise. They have begun to believe that a turbulence in forex markets could be round the corner.

But the unstated reason is always around. Many countries have begun to suspect that holding too many US dollars as part of their reserves might be unwise. They have begun to believe that a turbulence in forex markets could be round the corner.

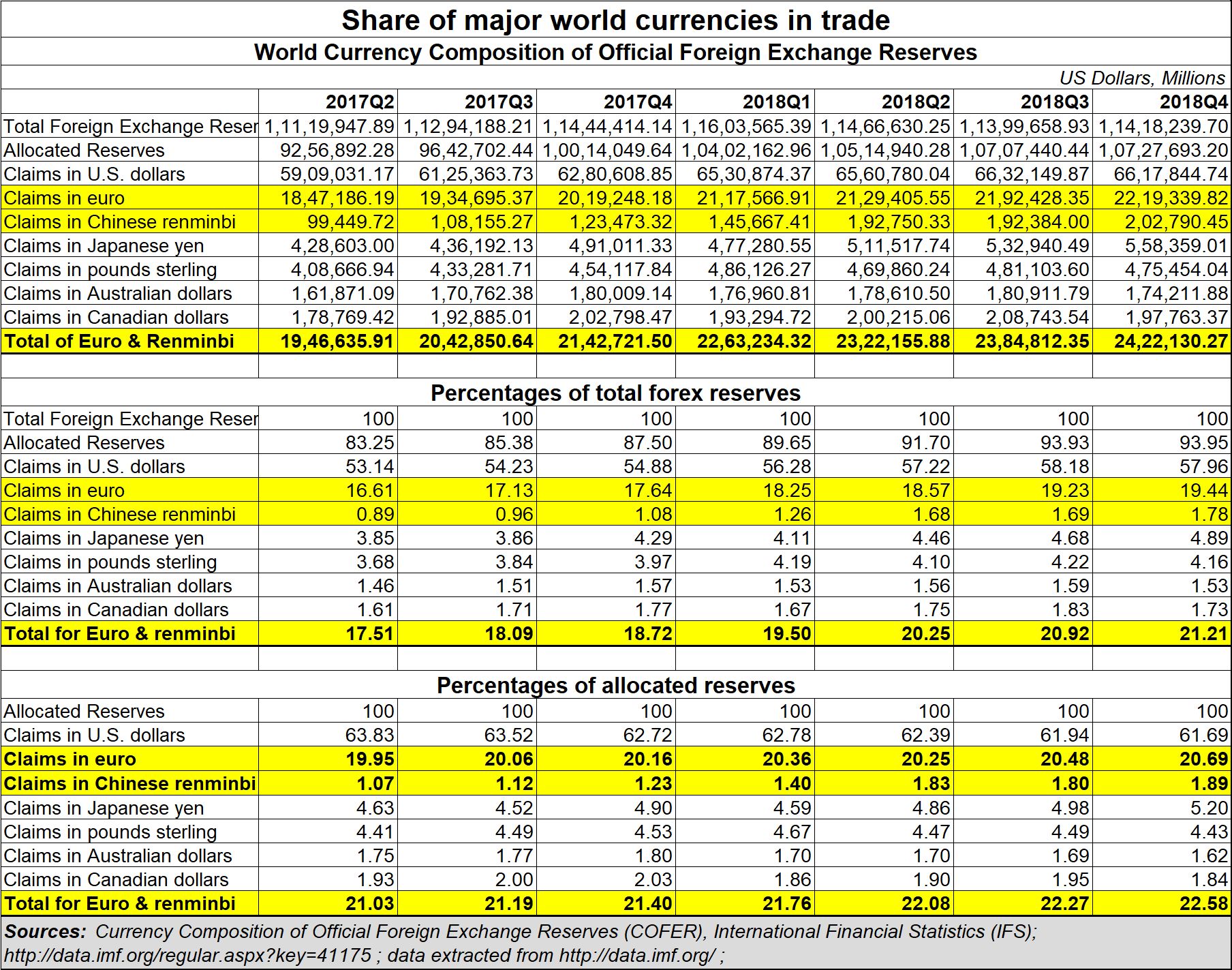

They point to the increasing role of non-dollar trades. While it is difficult to put a finger on the exact role each currency plays in world trade – some of the trades have in-built political gives-and-takes structured as part of such deals – a good indication can be found from figures released by Currency Composition of Official Foreign Exchange Reserves (COFER), International Financial Statistics (IFS) — http://data.imf.org/ and http://data.imf.org/regular.aspx?key=41175 . The numbers show that just Euro and  Renminbi trade swelled from 17.51% of total global foreign exchange reserves to 21.21% during just seven quarters from Q2 2017 to Q4 2018 (see table at http://www.asiaconverge.com/wp-content/uploads/2019/04/2019-04-27_Share-major-currencies-trade.jpg). But when allocated reserves (which are around 83-94% of total forex reserves) are taken into account, the share of the Euro and Renminbi soars even further. Their share climbed from 21.03% to 22.58% during the same period. This is without considering the Yen or the UK Pound, because they are unlikely to become global currencies. Clearly, the US dollar is losing its clout in global trade in a growing market.

Renminbi trade swelled from 17.51% of total global foreign exchange reserves to 21.21% during just seven quarters from Q2 2017 to Q4 2018 (see table at http://www.asiaconverge.com/wp-content/uploads/2019/04/2019-04-27_Share-major-currencies-trade.jpg). But when allocated reserves (which are around 83-94% of total forex reserves) are taken into account, the share of the Euro and Renminbi soars even further. Their share climbed from 21.03% to 22.58% during the same period. This is without considering the Yen or the UK Pound, because they are unlikely to become global currencies. Clearly, the US dollar is losing its clout in global trade in a growing market.

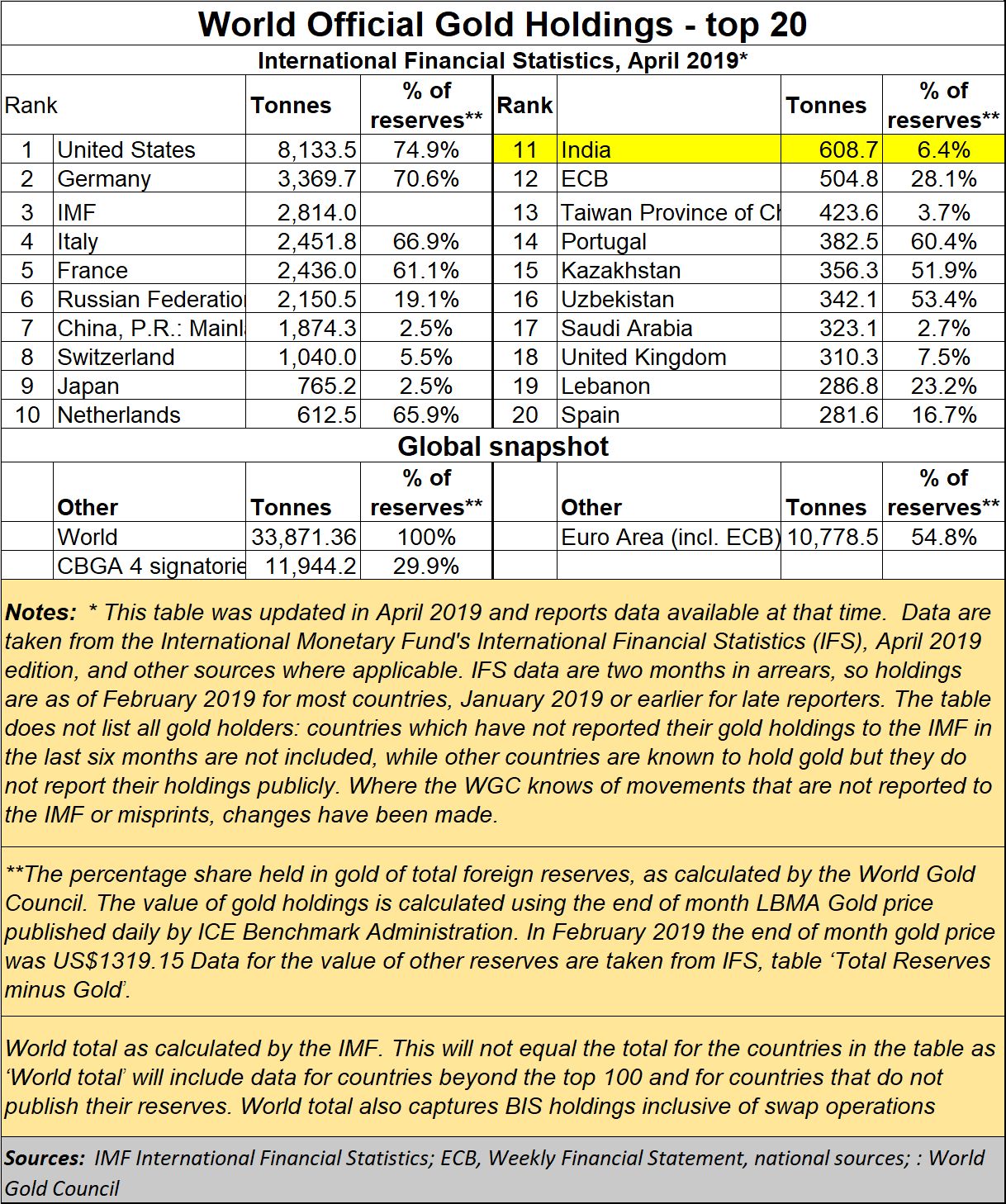

With neither the Euro nor the Renminbi yet ready to assume the mantle of becoming a global currency, many banks prefer reducing their exposure to the US dollar, and have begun focusing more on gold which is relatively neutral when it comes to geographic loyalties. However, the US, a major gold owning country, chose not to purchase gold during the past decade. It would appear that it did not want to give more weight to gold at the cost of its own global supremacy. Another major gold owner was Germany which actually sold 37 tonnes of gold. But that could be explained away because Germany already has too much of gold in its reserves.

In fact, both the US and Germany – both economic powerhouses in the global economy – have tremendous (though unstated) confidence in gold. This yellow metal already accounts for as much as 70.6% share in Germany’s forex reserves. The case of the US, it is even higher, at 74.9%. India’s holdings in gold stand at just 6.4% of its reserves. This low figure points to an urgent need for India to revise its gold policies and start building its gold reserves without resorting to global purchases. One way would be to liberalise gold mining policies (http://www.asiaconverge.com/2018/06/is-gold-mining-feasible-in-india/). Another way would be to introduce better versions of gold bonds (http://www.asiaconverge.com/2018/10/using-gold-bonds-to-reduce-cad/). After all, various estimates put India’s gold holdings (in private hands) at 20,000 tonnes to 25,000 tonnes, the largest in the world (http://www.asiaconverge.com/wp-content/uploads/2015/12/AConverge-Gold-booklet-ALL-low-res.pdf).

Expect both Russia and China to start scaling the list of top gold holders given their aggressive purchases during the past decade. Russia has an added advantage. It is believed to have the highest reserves of (as yet un-mined) gold in the world.

Also expect, the US dollar to continue losing its share in global commerce because of three reasons. First is obviously the emerging economic heft of China. Second is the stupid moves the US has itself made, explained a bit later A third reason could be the losing relevance of oil, thanks to solar and other renewable sources of energy. It is always worth remembering that the US is a major player in oil markets as well, both directly as well as through its various oil companies.

That the US has made unwise moves can be seen from the manner in which the US tried to sanction oil exports from Russia to Europe. That move made Russia swiftly clinch an oil and gas trade deal with China and build an oil pipeline to this dragon country. That, in turn reduced China’s vulnerability to both Middle East and US based energy markets, and caused a substantial amount of trade to move away from US dollars.

A similar situation is happening with Iran as well. Trying to impose (unilateral) sanctions against Iranian oil, will replay a similar scenario. It will push Iran to sell more oil to China, which always needs increasing amounts of energy as it grows in industrial strength. That will reduce the share of US dollar denominated trade further.

It won’t be long before India too might have to move this way, if it wants to bridge the growing trade balance with China which has already emerged as its largest trading partner. As time goes by, trade between India and China is bound to grow – partly on account of geographical proximity, much in the same way US-Canada trade ties have swelled over the past several decades, and partly because of business negotiations.

India’s defence deals with Russia are also likely to reduce dollar denominated trade, and this scenario could get replicated in several ways around the globe. China’s predominance in the telecom sector – remember 5G – could further accelerate the move away from the US dollar (http://www.asiaconverge.com/2019/03/china-paints-a-more-pleasing-visage-for-companies-and-investors/). That could also explain the ire of the US over China’s Belt and Road Initiative (BRI) which again gets into non-dollar deals.

As the dollar loses market share, expect turbulence in currency markets to increase. That will push more central banks towards gold.

Will this mean a gold rush? That is hard to say because gold prices are also a result of hedging and de-hedging strategies adopted by gold mining companies.

But one thing is certain. Gold is becoming more relevant to central banks than a decade ago. The lust for gold will thus remain undiminished.

{kind=link}

COMMENTS